Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

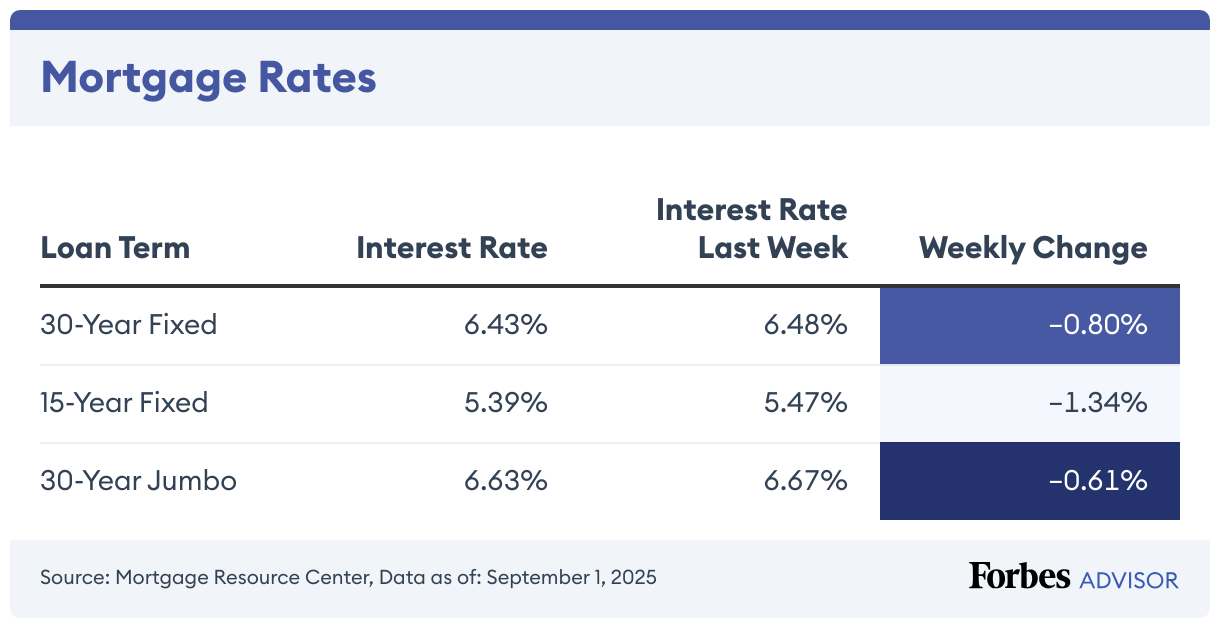

Thirty-year mortgage rates fell to a one-month low today. The current average mortgage rate on a 30-year fixed mortgage is 6.19%, compared to 6.25% a week earlier, according to the Mortgage Research Center.

For borrowers who want a shorter mortgage, the average rate on a 15-year fixed mortgage is 5.35%, down 0.60% from the previous week.

Homeowners who want to lock in a lower rate by refinancing should compare their existing mortgage rate to today’s refinance rates.

30-Year Mortgage Rates Drop 1.07%

Today’s 30-year mortgage—the most popular mortgage product—is 6.19%, down 1.07% from a week earlier.

The interest rate is just one fee included in your mortgage. You’ll also pay lender fees, which differ from lender to lender. Both interest rate and lender fees are captured in the APR. This week the APR on a 30-year fixed-rate mortgage is 6.21%. Last week, the APR was 6.28%.

Let’s say your home loan is $100,000 and you have a 30-year, fixed-rate mortgage with the current rate of 6.19%, your monthly payment will be about $612, including principal and interest (taxes and fees not included), the Forbes Advisor mortgage calculator shows. That’s around $120,793 in total interest over the life of the loan.

15-Year Mortgage Rates Drop 0.60%

Today’s 15-year mortgage (fixed-rate) is 5.35%, down 0.60% from the previous week. The same time last week, the 15-year, fixed-rate mortgage was at 5.38%.

The APR on a 15-year fixed is 5.39%. It was 5.42% a week earlier.

A 15-year, fixed-rate mortgage with today’s interest rate of 5.35% will cost $809 per month in principal and interest on a $100,000 mortgage (not including taxes and insurance). In this scenario, borrowers would pay approximately $46,036 in total interest.

Jumbo Mortgage Rates Climb 0.03%

The average interest rate on the 30-year fixed-rate jumbo mortgage (mortgages above 2025’s conforming loan limit of $806,500 in most areas) jumped up to 6.35%. Last week, the average rate was 6.34%.

Borrowers with a 30-year fixed-rate jumbo mortgage with today’s interest rate of 6.35% will pay $622 per month in principal and interest per $100,000. That means you’d pay around $124,287 in total interest over the life of the loan.

Trends in Mortgage Rates for 2025

After reaching 7.04% in January, the average interest rate for a 30-year fixed mortgage has steadily remained in the mid-to-high 6% range. The 15-year fixed mortgage rate has hovered between the low-6% and mid-to-high 5% range since its January peak of 6.27%.

Rates have trended downward since mid-January 2025, but experts aren’t forecasting further significant decreases in 2025. Rate drops may continue in 2026, especially if the Federal Reserve continues to cut the federal funds rate down.

When Will Mortgage Rates Go Down?

Mortgage rates are influenced by various economic factors, making it difficult to predict when they will drop.

Mortgage rates follow U.S. Treasury bond yields. When bond yields decrease, mortgage rates generally follow suit.

The Federal Reserve’s decisions and global events also play a key role in shaping mortgage rates. If inflation rises or the economy slows, the Fed may lower its federal funds rate. For example, during the Covid-19 pandemic, the Fed reduced rates, which drove interest rates to record lows.

A significant drop in mortgage rates seems unlikely in the near future. However, they may decline if inflation eases or the economy weakens.

How To Calculate Mortgage Payments

To get an estimate of your mortgage costs, using a mortgage calculator can help.

Simply input the following information:

- Home price

- Down payment amount

- Interest rate

- Loan term

- Taxes, insurance and any HOA fees

Find the Best Mortgage Lenders

How Are Mortgage Rates Determined?

Multiple factors affect the interest rate for a mortgage, including the economy’s overall health, benchmark interest rates and borrower-specific factors.

The Federal Reserve’s rate decisions and inflation can influence rates to move higher or lower. Although the Fed raising rates doesn’t directly cause mortgage rates to rise, an increase to its benchmark interest rate makes it more expensive for banks to lend money to consumers. Conversely, rates tend to decrease during periods of rate cuts and cooling inflation.

Home buyers can make several moves to improve their finances and qualify for competitive rates. One is having a good or excellent credit score, which ranges from 670 to 850. Another is maintaining a debt-to-income (DTI) ratio below 43%, which implies less risk of being unable to afford the monthly mortgage payment.

Further, making a minimum 20% down payment can help you avoid private mortgage insurance (PMI) on conventional home loans. If you can afford the larger monthly payment, 15-year home loans have lower rates than a 30-year term.

Find the Best Mortgage Lenders

Frequently Asked Questions (FAQs)

How do you get a lower mortgage interest rate?

Comparing lenders and loan programs is an excellent start. Borrowers should also strive for a good or excellent credit score between 670 and 850 and a debt-to-income ratio of 43% or less.

Further, making a minimum down payment of 20% on a conventional mortgage can help you automatically waive private mortgage insurance premiums, which increases your borrowing costs. Buying discount points or lender credits can also reduce your interest rate.

Will interest rates ever go back to 3%?

The Federal Reserve’s efforts to stabilize the economy during the Covid-19 pandemic drove the historically low rates. As the economy recovers, the unemployment rate decreases and inflation is controlled, rates may dip below current levels, but they’re unlikely to fall as low as 3% again anytime soon.

Should I choose a fixed- or adjustable-rate mortgage?

Choosing between a fixed- or adjustable-rate mortgage (ARM) depends on your financial situation. A fixed-rate mortgage suits those who want consistent monthly payments throughout the loan term without worrying about fluctuations in their rate or payments in response to market changes. If mortgage rates are low, securing a fixed rate can save you money in the long run.

An ARM, on the other hand, may appeal to those who want a lower initial rate and monthly payment. However, you also run the risk of ending up with higher payments if your rate fluctuates. If you expect your income to rise, you may feel confident handling these potential payment increases. These mortgages can also work well for those who plan to live in a home for only a few years, as you might sell or move before the rate adjusts.