Our Picks for the Best Life Insurance for Seniors

Summary: Best Senior Life Insurance Companies

Our rate ratings are based on coverage amounts of $250,000, $500,000 and $1 million. We are displaying the middle of that range for summary purposes.

Our Picks for the Best Life Insurance for Seniors

Protective

BEST OVERALL

Protective

Max issue age for 10-year term life

AM Best financial strength rating

Compare quotes from participating carriers via Lifequotes.com

Our Expert Takes

Protective is a top-notch budget-friendly choice for seniors seeking life insurance. It offers superior cost competitiveness, meaning lower premiums, internal company charges and total cost of insurance than competitors. Low-cost cash value policies mean more money goes toward cash value accumulation.

We think retirement age seniors will appreciate Protective’s highly reliable policy illustrations, which help in good financial planning. And its term life insurance plans offer very competitive rates.

Pros & Cons

- Classic Choice term life insurance rates for seniors are very competitive.

- You can renew the Classic Choice policy up to age 95 after your level term period ends.

- Its cash value policies for seniors generally have low internal costs.

- Protective has superior financial stability, indicating that seniors can have confidence in its ability to pay claims.

- Low internal costs.

- Highly reliable policy illustrations.

- Easy to access help through a toll-free number.

- The performance of Protective’s investment has historically been average.

- Cash value accumulation during the early years of Protective’s cash value policies may be slow.

- It is difficult to find policy-specific details on the company’s website.

Types of Life Insurance & Riders Available

Types of Life Insurance Sold

- Term life

- Whole life

- Universal life

- Indexed universal life

- Variable universal life

Life Insurance Riders Available

- Accidental death benefit rider

- Child life insurance rider

- Chronic illness rider

- Conversion choice with chronic illness rider

- Disability rider

- Guaranteed insurability rider

- Income protection rider

- Lapse protection rider

- Overloan protection rider

- Protected insurability rider

- Return of premium rider

- Terminal illness accelerated death benefit rider

- Waiver of premium rider

Availability of riders could depend on the type of policy.

More Insight

Seniors on a fixed income generally seek a good bang for their buck and financial safety and security in their later years. Protective’s life insurance policies can therefore be great for seniors due to costs that are among the lowest and most stable in the entire market, reliable quotes and illustrations and generally good access to cash value in case of emergencies without adversely affecting income-producing assets.

– Barry D. Flagg, advisory board member

Pacific Life

BEST FOR INVESTMENT PERFORMANCE

Pacific Life

Max issue age for 10-year term life

AM Best financial strength rating

Compare quotes from participating carriers via Lifequotes.com

Our Expert Takes

Pacific Life stands out for seniors because of the superior performance of its investments, which fuel cash value. We also appreciate that the high reliability of its policy illustrations gives retirees trustworthy projections of how their life insurance policy will perform.

We like that Pacific Life is budget-friendly and offers competitive rates through its PL Promise Term, for seniors seeking term life. Plus, the policy is renewable up to age 95 after the level term period ends.

Pros & Cons

- Superior rates for term life insurance for seniors.

- Excellent historical investment performance.

- Policy illustrations for Pacific Life’s cash value policies tend to be reliable.

- Many of Pacific Life’s policies can build cash value even in the early years.

- It is easy to access a Pacific Life representative through a contact form or toll-free number.

- The cost competitiveness of its cash value policies for seniors is OK, but some competitors deliver lower policy costs.

- Conversion is limited only to universal life insurance.

Types of Life Insurance & Riders Available

Types of Life Insurance Sold

- Term life

- Whole life

- Fixed-rate universal life

- Indexed universal life

- Variable universal life

Life Insurance Riders Available

- Additional insurance rider

- Child life insurance rider

- Chronic illness rider

- Early/enhanced cash value rider

- Estate protection rider

- Lapse protection rider

- Long term care rider

- Overloan protection rider

- Return of premium rider

- Spouse/other insured rider

- Terminal illness accelerated death benefit rider

- Waiver of monthly deduction rider

Availability of riders could depend on the type of policy.

More Insight

Pacific Life has a good history of offering policies with low costs and competitive investment options. But costs in some newer cash value policies can be high. Plus, some newer investment options have not been meeting expectations. If you’re considering a Pacific Life cash value policy be sure to ask your financial advisor 1) whether internal policy costs are higher or lower than industry benchmarks and 2) for the actual track record of the recommended investment options (not just hypothetical projections).

– Barry D. Flagg, advisory board member

Minnesota Life

BEST FOR FINANCIAL STRENGTH

Minnesota Life

Max issue age for 10-year term life

A.M. Best financial strength rating

Our Expert Takes

Minnesota Life should appeal to seniors who are buying life insurance because of its excellent financial strength. Solid financial strength can give seniors the assurance that approved claims on their policy will be paid. We also like that their long-term care options include the ability to cover care provided by a family member.

Pros & Cons

- Superior financial strength.

- Low level of complaints.

- Term rates are competitive for 10-year, $250,000 policies for females.

- Policy-specific details are difficult to find on the company’s website.

- Term life rates are significantly higher than other top competitors for most shoppers.

- No online quotes.

Types of Life Insurance & Riders Available

Types of Life Insurance Sold

- Term life

- Indexed universal life

- Variable universal life

Life Insurance Riders Available

- Chronic illness rider

- Early values agreement

- Exchange of insureds rider

- Extended conversion rider

- Guaranteed insurability rider

- Income protection rider

- Inflation rider

- Overloan protection rider

- Premium deposit account rider

- Terminal or chronic illness accelerated death benefit rider

- Waiver of premium rider

Availability of riders could depend on the type of policy.

How Much Does Senior Life Insurance Cost?

The average yearly cost of a 10-year term life policy for healthy 70-year-old adults ranges from $1,196 to well over $9,355. Which end of that range you should expect depends on factors like your age, health, smoking status, the type and amount of coverage you buy and the insurance company you choose.

Here’s a look at term life insurance quotes for 70-year-old buyers of senior life insurance from the top ranking companies in our analysis.

Seniors over 70 will find it difficult to buy 20-year term life insurance and likely won’t be able to find a 30-year term life insurance policy at all, so we’ve provided you rates for a 10-year term.

Senior Life Insurance Costs for Females

Senior Life Insurance Costs for Males

Types of Life Insurance for Seniors

Senior life insurance buyers can choose among the same types of life insurance as anyone else. All of Forbes Advisor’s top-rated life insurance companies for seniors offer term, cash value and no-exam life insurance.

Term Life Insurance

Term life insurance for seniors is often available through age 80, although the length of the level term period available will get shorter as you get older. For example, at age 80, your longest option will likely be 10-year term life insurance. You may also be limited on coverage amounts at an older age and be required to get a life insurance medical exam.

Cash Value Life Insurance

Cash value policies such as whole life insurance and universal life insurance can be obtained with some companies through age 85, but some insurers have lower maximum ages. We did not find cash value policies available for people over 85. Monthly costs for cash value life insurance and required medical exams can become a hurdle at older ages.

No-Exam Life Insurance

No-exam life insurance for seniors is generally available in two forms: Guaranteed life insurance or burial insurance. A guaranteed issue life insurance policy has no medical exam or questions. These are an option for someone who is older and/or is in poor health.

Burial insurance, or final expense insurance, is generally a small whole life insurance policy (such as $5,000 to $25,000) intended to cover only funeral costs. It may be a guaranteed life insurance policy.

Get Instant Life Insurance Quotes from Top Insurers

Compare Policies Hassle-Free, No Login

Cheapest Life Insurance for Seniors

Based on our analysis, Penn Mutual and Transamerica are the cheapest life insurance companies for healthy 70-year-old buyers. These companies had the most inexpensive rates for term life insurance for 70-year-old seniors among the companies we analyzed.

However, it is important to understand that personal health and other details impact cost, and affordability for retired seniors may look different than for those working.

No one company will offer cheap life insurance for every individual.

Cheapest Life Insurance for Seniors: 70-Year-Old Female Buyers

Rates are based on buyers in excellent health.

Cheapest Life Insurance for Seniors: 70-Year-Old Male Buyers

Rates are based on buyers in excellent health.

Is Life Insurance for Seniors Worth It?

Senior life insurance can be worth it when its payout will:

- Help beneficiaries pay for expenses such as funeral costs, medical bills and remaining debts.

- Provide funds for your spouse to live off of if you were living on a pension that doesn’t have survivor benefits.

- Provide an inheritance to your children, grandchildren or others.

- Help heirs pay estate taxes on large estates.

We Answer Your Questions

Ashlee Valentine

Insurance Editor

Les Masterson

Insurance Editor

Michelle Megna

Insurance Lead Editor

I am turning 75 next month and am regretting that I’ve never purchased life insurance. Is it too late?

– Robert M., Dayton, Ohio

Although your options will be limited and pricey, buying life insurance at or over 75, you can still purchase a guaranteed issue policy. Those policies come with guaranteed approval but low coverage amounts, graded death benefits and high premiums.

If I access my living benefits now to help with long-term care, how will this affect my death benefit?

– Walter R., Lexington, Kentucky

When you access your life insurance policy’s living benefits, you are accessing your death benefit early. That means any use of living benefits will decrease the death benefit that will be paid to your beneficiaries.

What happens if my life insurance beneficiary dies before I do?

– Albert R., Laramie, Wyoming

If your primary beneficiary dies and you have specified a contingent beneficiary, the payout will go to that person. If you do not have any other beneficiaries listed in the policy, the payout will go to your estate. If your death benefit goes into your estate, it can be subject to estate taxes and creditor claims. So, if your primary or contingent beneficiary passes away, it’s smart to name someone else on the policy.

Related: Is Life Insurance Worth It?

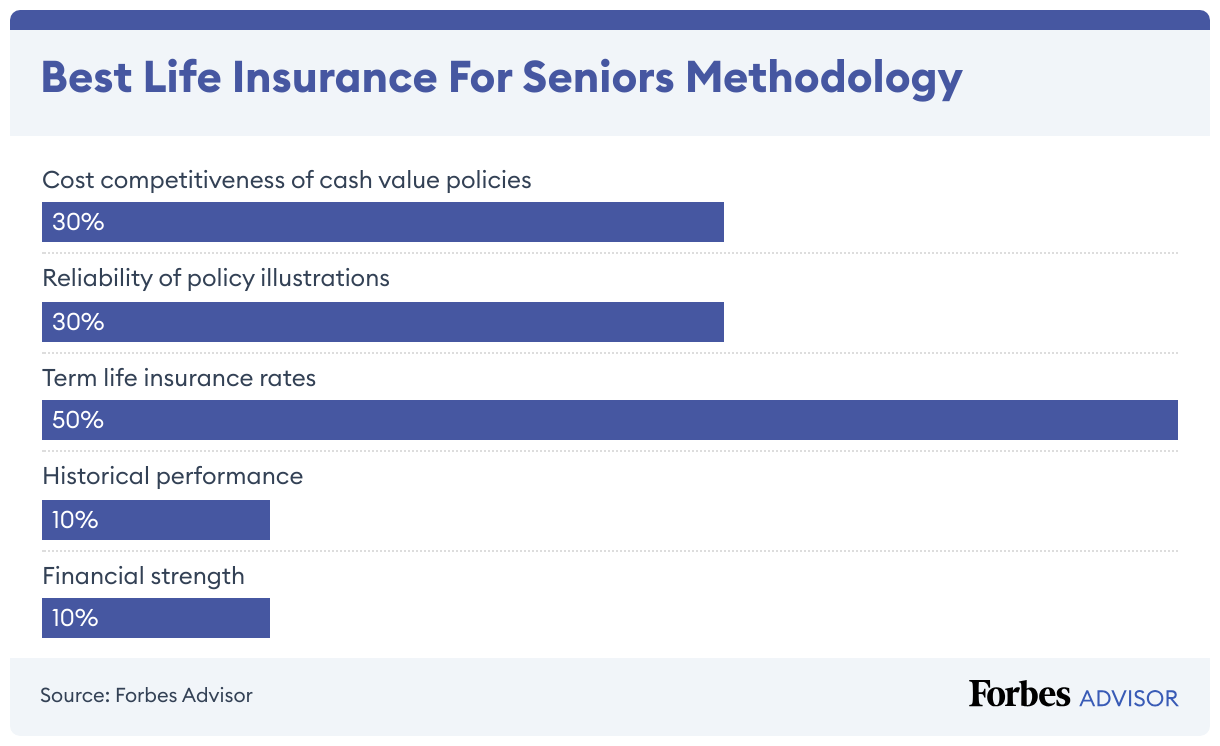

Methodology

To find the best life insurance for seniors, we evaluated both term life and permanent life insurance:

- For term life insurance analysis, we used our own research.

- For cash value life insurance analysis, we used data provided by Veralytic, an independent publisher of life insurance research and analytics. Veralytic measures the competitiveness of permanent life insurance products and can provide a customized policy analysis to your financial advisor.

Our ratings are based on:

Cost competitiveness of cash value policies (30% of score): This measures the level of premiums and internal policy charges for seniors, including the cost of insurance, fixed administration expenses and cash value-based wrap fees.

Reliability of policy illustrations (30% of score): We evaluated the reliability over time of the company’s illustrations for senior policyholders for permanent life insurance products.

Term life insurance rates (20% score): We used term life insurance rates for healthy buyers at age 70 for 10-year term life with coverage of $250,000, $500,000 and $1 million.

Historical performance (10% of score): This measures the historical performance of the company’s investments that fuel cash value growth.

Financial strength (10% of score): This measure incorporates the insurer’s financial strength ratings from four major ratings agencies: AM Best, Fitch, Moody’s and Standard and Poor’s.

Read more: How Forbes Advisor rates life insurance companies

Best Senior Life Insurance Frequently Asked Questions (FAQs)

Is there an age limit to buy life insurance?

Life insurance companies set maximum age limits, depending on the type of policy. For example, for Corebridge Financial’s Select-a-Term policy, the maximum issue age is 80 while Equitable’s maximum issue age for a 10-year term is 75. If you are over 80, guaranteed issue policies will most likely be your only option.

The younger you can buy life insurance, the more policy options you’ll have to compare.

At what age should you stop buying life insurance?

The need for life insurance doesn’t end upon reaching a certain age. Certain types of life insurance may even include long term care benefits to assist with senior care. But here are some situations where it makes sense to cancel your life insurance policy:

-

-

- The cost outweighs the death benefit that will be paid to your beneficiaries.

- Your financial status has changed, and the death benefit will no longer be needed to cover debts, income or final expenses.

-

Are there life insurance policies designed specifically for seniors?

These two policy types are especially for senior life insurance buyers:

Guaranteed issue life insurance. These policies are offered with the promise that you can’t be turned down and won’t be asked any health questions. The trade-off is that maximum coverage amounts tend to be small, and if you die in the first two or three years after purchase your beneficiaries won’t get the full death benefit. This is known as a graded death benefit.

Guaranteed issue life insurance is pricey for the amount of insurance you’re getting, but it’s designed for seniors who have health issues.

Burial insurance. Also known as final expense insurance, burial insurance is available only in small amounts and is designed for seniors in poor health and with limited budgets. It’s meant to cover a funeral and final expenses.

What is the best life insurance for a senior in poor health?

You can buy a guaranteed issue life insurance plan without any health questions or an exam. These policies offer low amounts of coverage but are designed for people looking to cover a funeral and other smaller expenses.

Note that guaranteed issue policies have “graded death benefits.” If you pass away within the first two or three years of owning the policy, the death benefit will not be paid to your beneficiaries. Instead, the policy will usually refund your premiums plus interest.

Why is life insurance more expensive for seniors?

Life insurance companies assess risk to determine life insurance rates. The company’s likelihood of paying out a death benefit for your policy increases as you age, and they charge a higher premium to make up for the higher risk. Seniors are also more likely to have chronic health conditions, increasing the risk of death. If you’re a senior buying a policy for yourself, or you’re buying a policy for older parents, you should expect higher rates.