Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

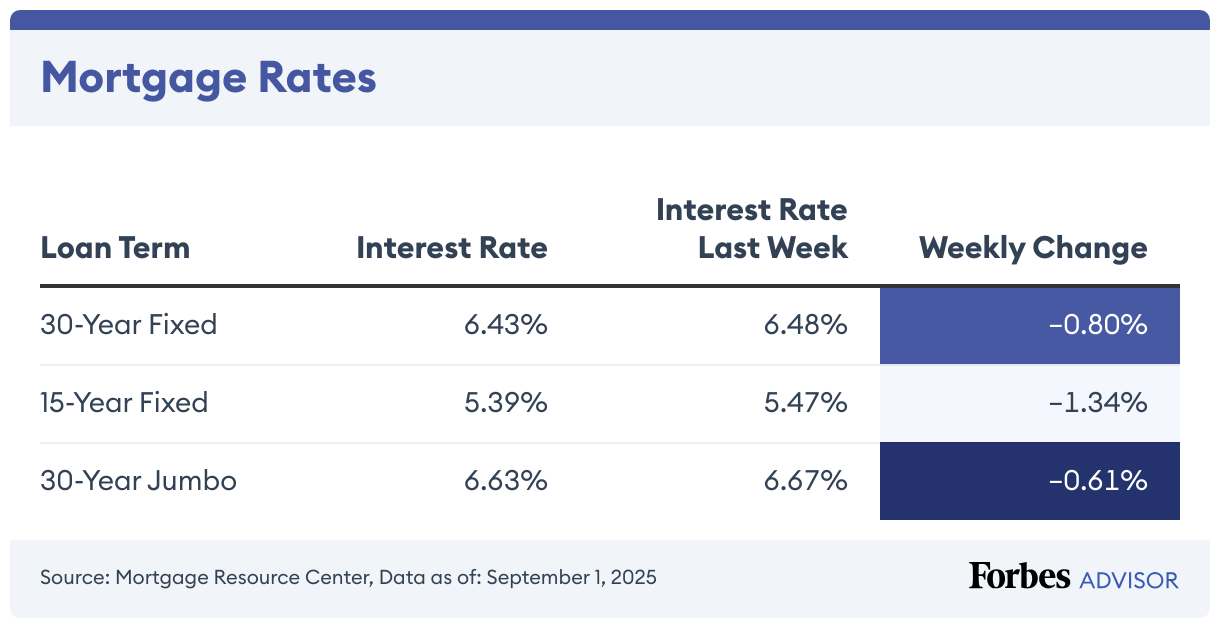

Currently, the average interest rate on a 30-year fixed mortgage is 6.28%, compared to 6.37% a week ago, according to the Mortgage Research Center.

For borrowers who want to pay off their home faster, the average rate on a 15-year fixed mortgage is 5.40%, down 1.05% from the previous week.

Homeowners who want to lock in a lower rate by refinancing should compare their existing mortgage rate with current market rates to make sure it’s worth the cost to refinance.

30-Year Mortgage Rates Drop 1.30%

Today’s 30-year mortgage—the most popular mortgage product—is 6.28%, down 1.30% from a week earlier.

The interest rate is just one fee included in your mortgage. You’ll also pay lender fees, which differ from lender to lender. Both interest rate and lender fees are captured in the APR. This week the APR on a 30-year fixed-rate mortgage is 6.31%. Last week, the APR was 6.4%.

Let’s say your home loan is $100,000 and you have a 30-year, fixed-rate mortgage with the current rate of 6.28%, your monthly payment will be about $618, including principal and interest (taxes and fees not included), the Forbes Advisor mortgage calculator shows. That’s around $123,135 in total interest over the life of the loan.

15-Year Mortgage Rates Drop 1.05%

The average interest rate on a 15-year mortgage (fixed-rate) declined to 5.4%. This same time last week, the 15-year fixed-rate mortgage was at 5.45%.

The APR on a 15-year fixed is 5.44%. It was 5.5% this time last week.

At today’s interest rate of 5.4%, a 15-year fixed-rate mortgage would cost approximately $812 per month in principal and interest per $100,000. You would pay around $46,541 in total interest over the life of the loan.

Jumbo Mortgage Rates Climb 0.40%

Today’s average interest rate on a 30-year fixed-rate jumbo mortgage (a mortgage above 2025’s conforming loan limit of $806,500 in most areas) climbed 0.40% from last week to 6.76%.

Borrowers with a 30-year, fixed-rate jumbo mortgage with today’s interest rate of 6.76% will pay approximately $649 per month in principal and interest per $100,000 borrowed. That would be $134,214.

Trends in Mortgage Rates for 2025

After reaching 7.04% in January, the average interest rate for a 30-year fixed mortgage has steadily remained in the mid-to-high 6% range. The 15-year fixed mortgage rate has hovered between the low-6% and mid-to-high 5% range since its January peak of 6.27%.

Rates have trended downward since mid-January 2025, but experts aren’t forecasting further significant decreases in 2025. Rate drops may continue in 2026, especially if the Federal Reserve continues to cut the federal funds rate down.

When Can I Expect Mortgage Rates To Drop?

Various economic factors influence mortgage rates, making it challenging to forecast when rates will drop.

The Federal Reserve’s decisions significantly impact mortgage rates. In response to inflation or an economic downturn, the Fed may lower its federal funds rate, prompting lenders to reduce mortgage rates.

Mortgage rates also track U.S. Treasury bond yields. If bond yields drop, mortgage rates typically follow suit.

Finally, global events that cause financial disruptions can affect mortgage rates. For example, the Covid-19 pandemic led to record-low interest rates when the Fed cut rates.

While a significant decrease in mortgage rates is unlikely in the near future, they may start to decline if inflation eases or the economy weakens.

What Affects Mortgage Rates?

The Federal Reserve’s restrictive monetary policy – including its interest rate hikes, which it’s using to restrain inflation – is the primary factor that’s pushing long-term mortgage rates higher. The state of the economy and housing market also affects mortgage rates. As for what interest rate the lender might offer you, this depends on your debt-to-income (DTI) ratio and credit score, both of which indicate your risk as a borrower.

Related: Mortgage Rates Forecast And Trends

How To Compare Mortgage Rates

Shop around and talk to various lenders to get a sense of each company’s mortgage loan offerings and services. Don’t go with the first lender quote you receive; instead, compare the best mortgage rate quotes to get a deal. In particular, consider what fees they charge, what fees they’re willing to waive and what closing assistance they might provide. Make sure any special offers or discounts don’t come at the cost of a higher mortgage rate.

Be sure to apply with each lender within a 45-day window. During this window, you can have multiple lenders pull your credit history without additional impact on your credit score.

Is This a Good Time To Buy a House?

Mortgage rates remain elevated, and the nation’s housing supply remains limited. The low inventory is preventing house prices from dropping. Meanwhile, the combination of high mortgage rates and appreciated home values will continue to present an obstacle for many prospective homebuyers seeking affordable housing.

Find the Best Mortgage Lenders of 2025

How Are Mortgage Rates Determined?

Home loan borrowers can qualify for better mortgage rates by having good or excellent credit, maintaining a low debt-to-income (DTI) ratio and pursuing loan programs that don’t charge mortgage insurance premiums or similar ongoing charges that increase the loan’s APR.

Comparing rates from different mortgage lenders is an excellent starting point. You may also compare conventional, first-time homebuyer and government-backed programs like FHA and VA loans, which have different rates and fees.

Several economic factors influence the trajectory of rates for new home loans. For example, Federal Reserve rate hikes indirectly cause the interest rates for many long-term loans to increase. Rates are more likely to decrease when the Fed pauses or decreases its benchmark Federal Funds Rate.

The inflation rate and the general state of the economy also impact interest rates. High inflation and a strong economy typically signal higher rates. Cooling consumer demand or inflation may lead to rate decreases.

Frequently Asked Questions (FAQs)

How do you get a lower mortgage interest rate?

Comparing lenders and loan programs is an excellent start. Borrowers should also strive for a good or excellent credit score between 670 and 850 and a debt-to-income ratio of 43% or less.

Further, making a minimum down payment of 20% on a conventional mortgage can help you automatically waive private mortgage insurance premiums, which increases your borrowing costs. Buying discount points or lender credits can also reduce your interest rate.

How long can you lock in a mortgage rate?

Most rate locks last 30 to 60 days and your lender may not charge a fee for this initial period. However, extending the rate lock period up to 90 or 120 days is possible, depending on your lender, but additional costs may apply.

What determines your interest rate?

National average interest rates depend on economic and market conditions, including the bond market, inflation, the economy and Federal Reserve decisions.

Lenders set rates based on the loan type and term. In general, shorter terms tend to come with lower rates. Additionally, making a larger down payment signals less risk to the lender, which could get you a better rate.

Other factors that can impact your rate include your credit score, debt-to-income (DTI) ratio, income and property location.