Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

Table of Contents

Find The Best Life Insurance

Find The Best Life Insurance

Compare Life Insurance Quotes

Summary: The Best Term Life Insurance Companies

The Best Term Life Insurance Companies

How Much Does a Term Life Insurance Policy Cost?

The average monthly cost is $19 for a $500,000 term life insurance policy for a buyer age 40 for a 10-year term, $29 for a 20-year term and $49 for a 30-year term. That’s $228 to $588 per year, depending on the term length.

Average Monthly Term Life Insurance Cost for a $500,000 Policy

Source: Forbes Advisor research. Rates are based on buyers who are healthy and qualify for the best rates.

Best Term Life Insurance Companies by Term

Term life insurance is offered by level term period, during which time the premiums are fixed and the death benefit is guaranteed. The level term periods offered vary by insurance company, but the best companies offer at least 10-, 20- and 30-year terms. The longer the term period, the higher the premium.

Using the top-ranking companies in our analysis, here are the lowest costs by level term. Actual rates will vary based on your age, health, coverage amount and other factors.

Best 10-Year Term Life Insurance

Best 20-Year Term Life Insurance

Best 30-Year Term Life Insurance

How Do I Find the Best Term Life Insurance?

Daniel Adams

Advisory board member

Ashlee Valentine

Insurance Editor

Amy Danise

Insurance Managing Editor

Penny Gusner

Insurance Senior Writer

Michelle Megna

Insurance Lead Editor

Jason Metz

Insurance Lead Editor

Get Life Insurance Pre-approval

If you have any health or risk concerns, ask your insurance agent to provide you with a preliminary approval from a company underwriter before going through the entire application process. This can give you a stronger assurance that you will get the offer you were quoted and help you avoid any unwelcome surprises when the official offer comes back.

Look Into Living Benefits

I recommend looking at whether any of the policies you’re considering have living benefits. This feature lets you take money from your own death benefit if you develop a chronic or critical illness that qualifies. It’s a great way to access a pool of money later that you can use for unexpected medical bills or other expenses.

Compare Life Insurance Quotes

I recommend comparing life insurance quotes from multiple companies. Find a good insurance agent or financial advisor who can gather quotes from multiple insurers. An experienced advisor will know which insurers are most likely to have competitive prices for your age and health.

Look For Term Life Conversion

If I’m looking for the best term life insurance, I’m going to shop mainly on price, but I’m also going to make sure the policy will let me convert to a cash value policy later on. This term life conversion option is a good way to hedge your bets. You may find you want a permanent life policy many years later, when buying a new policy could be cost-prohibitive.

Consider Temporary Life Insurance

You can usually attach a check to your term life application and get temporary life insurance while your application is being processed. If this option is available, why not take it and get peace of mind right away.

Check Into a Waiver Of Premium Rider

Consider adding a waiver of premium rider, depending on the cost. This rider will waive your life insurance payments if you become disabled and cannot work. Make sure to check the rules for what qualifies to use the rider.

Compare Life Insurance Companies

Compare Policies With Leading Insurers

Factors Affecting Term Life Insurance Rates

Life insurance companies usually look at these factors that affect term life insurance rates.

We Answer Your Questions

Ashlee Valentine

Insurance Editor

Penny Gusner

Insurance Senior Writer

Michelle Megna

Insurance Lead Editor

Should I consider inflation when determining how much life insurance coverage I need?

-Ellis R., Adel, Georgia

Inflation should be considered when selecting your life insurance coverage amount. Let’s say you’ve calculated a need of $500,000 coverage if you died today. If you die 20 years from now, however, the amount needed to cover the same financial needs will be different and likely higher. Work with your agent to make sure you’re accounting for inflation. The insurer may also offer an inflation rider.

I bought a 10-year term policy but now wish I bought a 30-year instead. Can I change my term?

– Cynthia L., Topeka, Kansas

Since the policy went through the underwriting process for a 10-year term, you cannot change the term now. You will need to apply for a new policy with a 30-year term and go through the underwriting process again. If you’re interested in switching to a permanent policy instead, check to see if your policy offers term life conversion.

What happens if I miss a payment on my term life policy?

– Jacob T., Sarasota, Florida

You are unlikely to lose your policy over one missed payment as most life insurance companies offer a 30- or 31-day grace period. But you do need to make the required premium payment during the grace period or your policy will lapse. If you know you’ll miss a payment, contact your insurance agent to discuss and make sure you understand the insurer’s grace period and policy reinstatement rules, if needed.

Compare Life Insurance Companies

Compare Policies With Leading Insurers

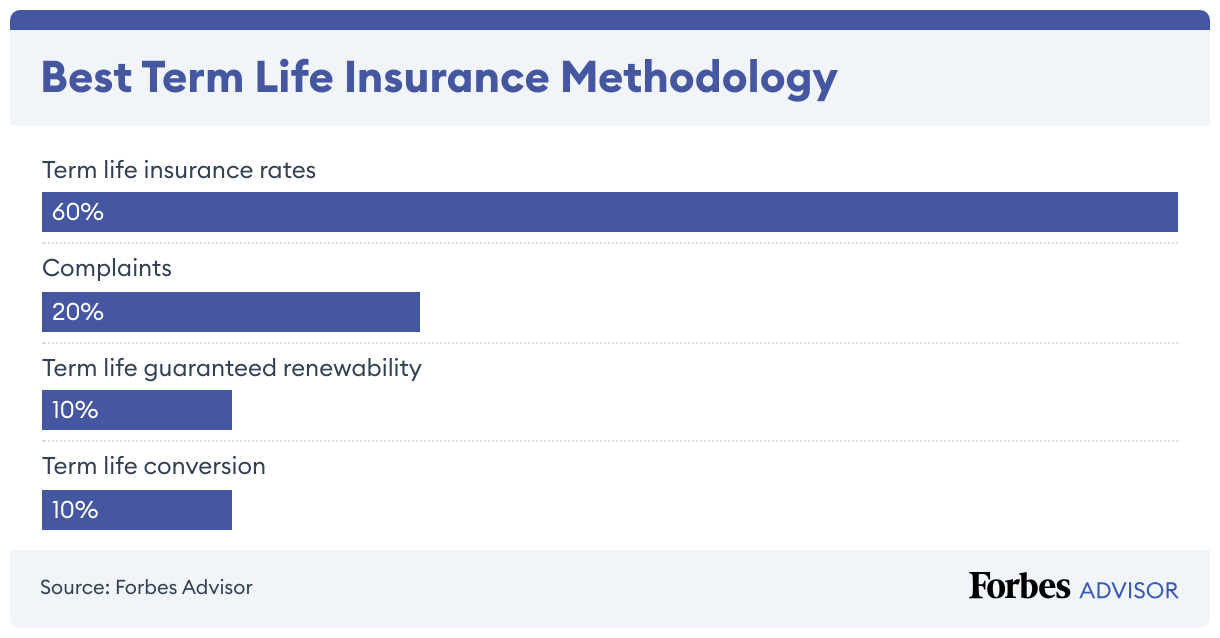

Methodology

To find the best term life insurance, we evaluated 20 companies on these measurements:

Read more: How Forbes Advisor rates life insurance companies

Other Term Life Insurance Companies We Rated

Best Term Life Insurance Frequently Asked Questions (FAQs)

Will taking a medical exam get me better term life insurance rates?

Taking a medical exam can potentially lead to better term life insurance quotes. Traditional life insurance policies with medical exams are considered lower risk for the insurer and may result in better rates if you are in good health, especially when compared to more expensive options like guaranteed issue life insurance.

But there are an increasing number of options for no-exam life insurance that have pricing that’s competitive with, or even lower than, policies that require a medical exam.

What is the maximum age for term life insurance?

The maximum issue age for term life insurance averages age 74, for a 10-year term life policy, according to a Forbes Advisor analysis of term life insurance companies. We found maximum issue ages ranging from 60 to 80.

What happens if you live beyond your life insurance term period?

If you outlive your life insurance term period, you can often renew the policy at a much higher premium (if that option is available). Or you can shop for a new life insurance policy.

If you don’t renew a term life insurance policy, your beneficiaries will not receive a death benefit payout if you die after the term expires.

Should I renew my term life policy when it ends?

Although renewing a term life insurance policy is convenient, it can get very expensive. Renewal rates are often significantly higher than the original level term rate and will continue to increase with each renewal.

Renewal can be a good option if you’ve developed a medical condition that will result in difficulty obtaining a new policy. But before you decide, check with your insurance agent to discuss your best options.

Learn More About Term Life Insurance

Forbes Advisor is not a licensed insurance agency. Insurance offerings are powered by Marketplace P&C LLC, NPN 20753534 and CA Lic. # 6011227.

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.